Understand annuities completely

Learn the real mechanics, not the brochure version. History, mathematics, products, limitations, and use cases in plain language.

The income architecture for the lifestyle you actually want. A serious, visual, plain language guide to annuities, lifetime income, Hybrid Retirement, and generational continuity.

The book is written for two readers at the same table: the Income Buyer who needs income for their own continued life, and the Generational Steward who wants a structure that can outlast them.

Learn the real mechanics, not the brochure version. History, mathematics, products, limitations, and use cases in plain language.

Separate architecture from product selection, ask better questions, and recognise when a recommendation does not fit your configuration.

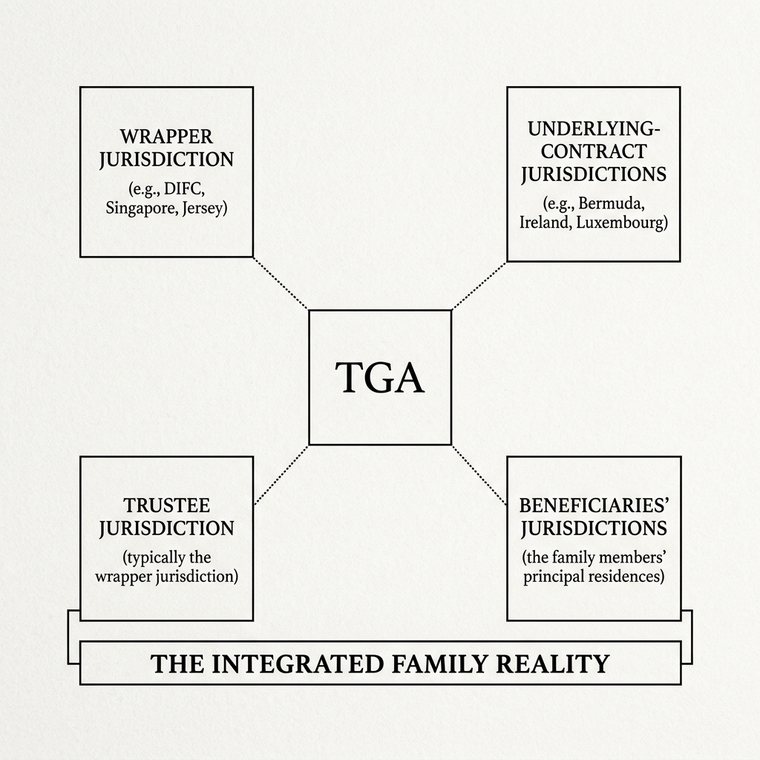

Move beyond retirement product thinking into family office applications, wrappers, trustee structures, and generational income design.

Hybrid Retirement begins when work becomes optional. The book shows what kind of life the income engine is actually buying.

A serious map of annuities as income architecture, moving from the human question to history, mathematics, product families, family office structures, and the lifestyle that lifetime income makes possible.

For the person asking how their own continued life will be funded, how work can become optional, and how income can be made less dependent on market timing.

For the family member, advisor, trustee, or principal designing structures that can outlast one person and support multiple generations.

Plain language answers to why annuities exist, how they work, when they appear in real lives, and what buyers should watch for.

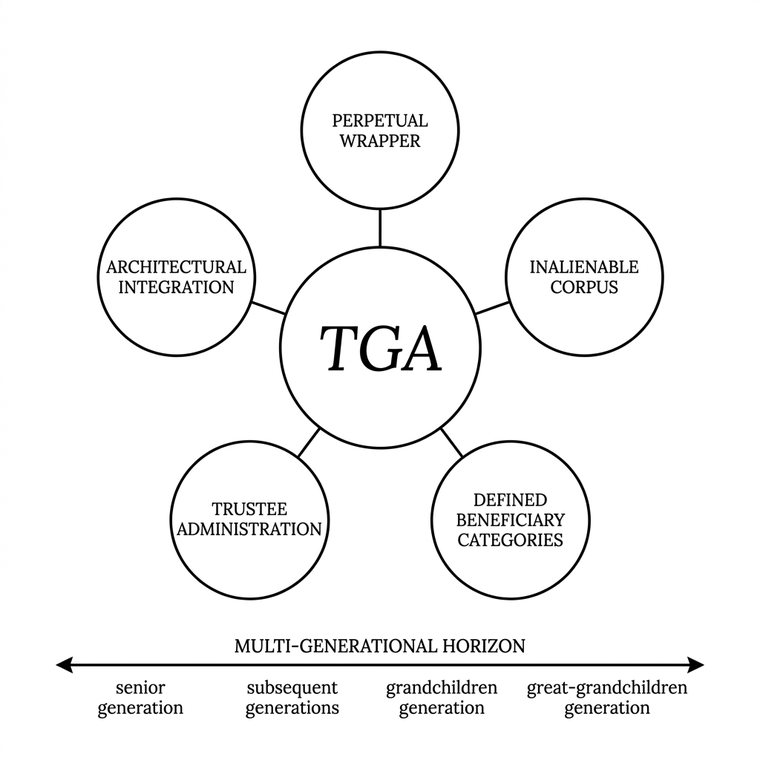

Roman annua, tontines, waqf, family estates, lineage trusts, and the two thousand year continuity of lifetime income arrangements.

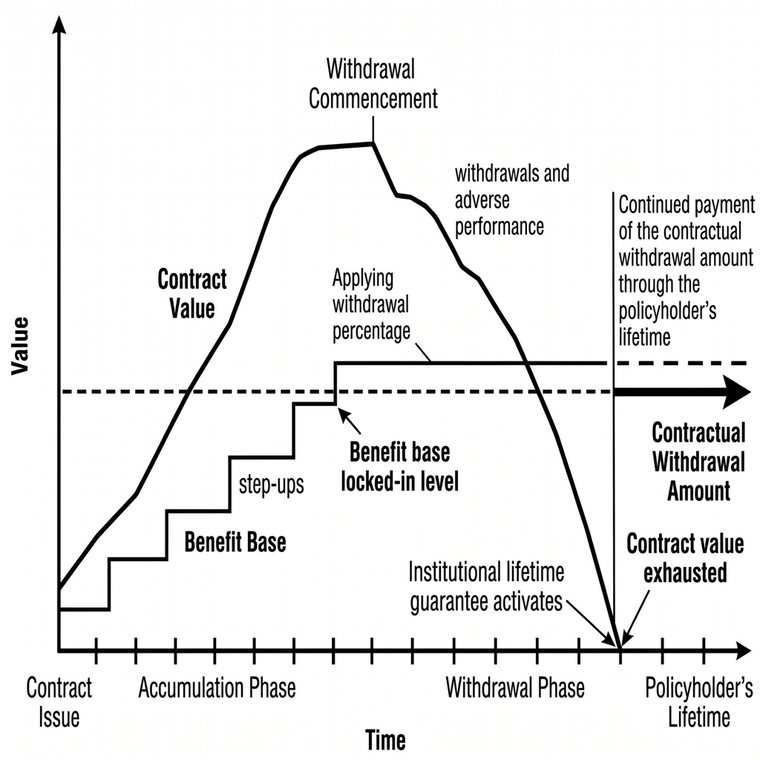

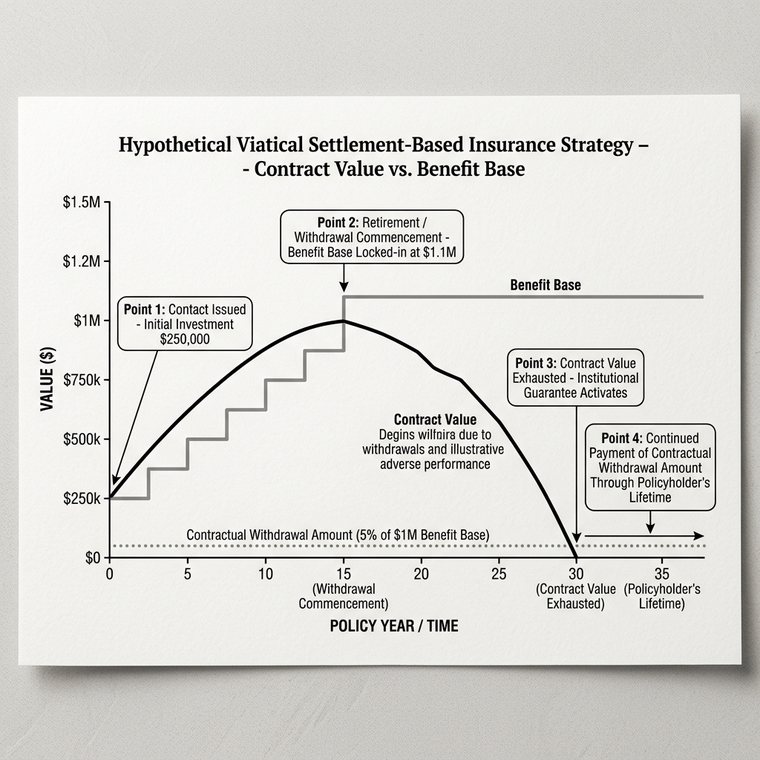

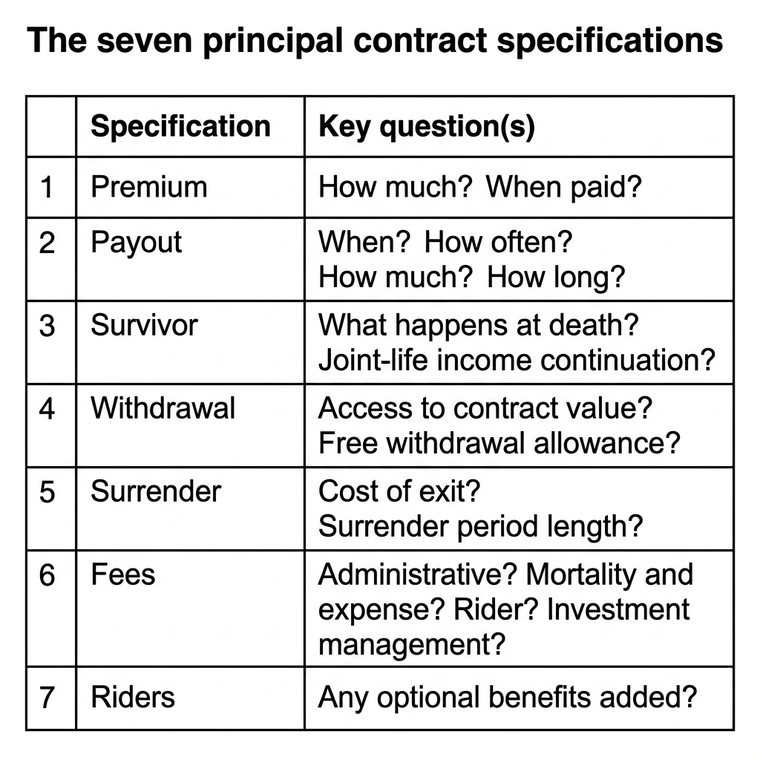

Mortality credits, longevity risk, sequence risk, decumulation, and the mechanics that make income pooling different from portfolio withdrawal.

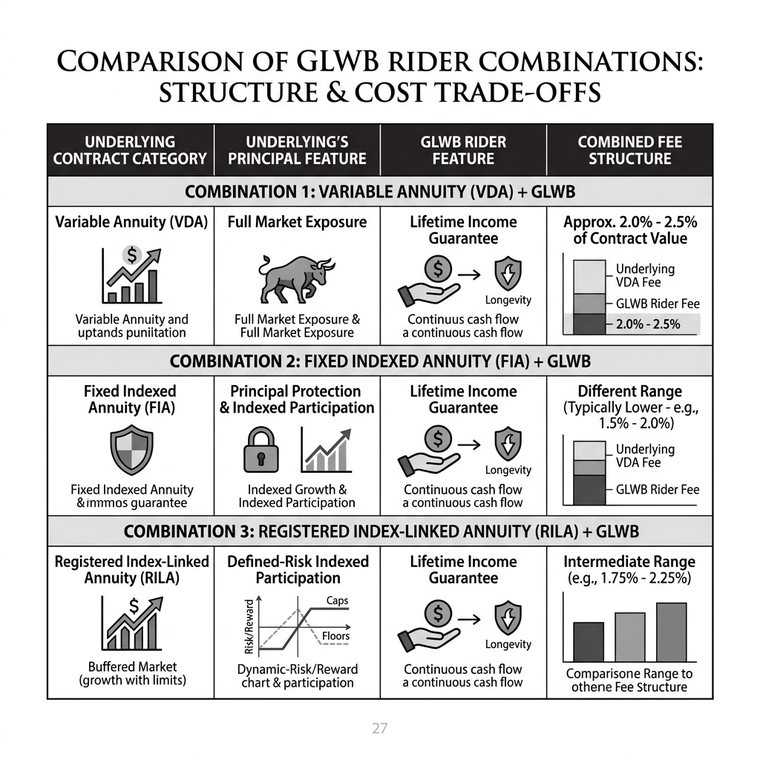

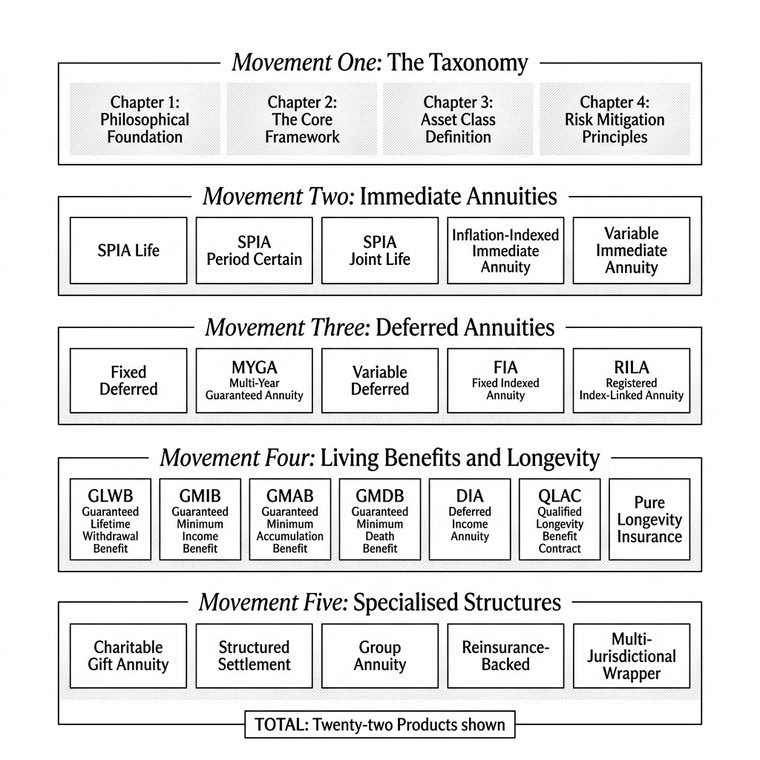

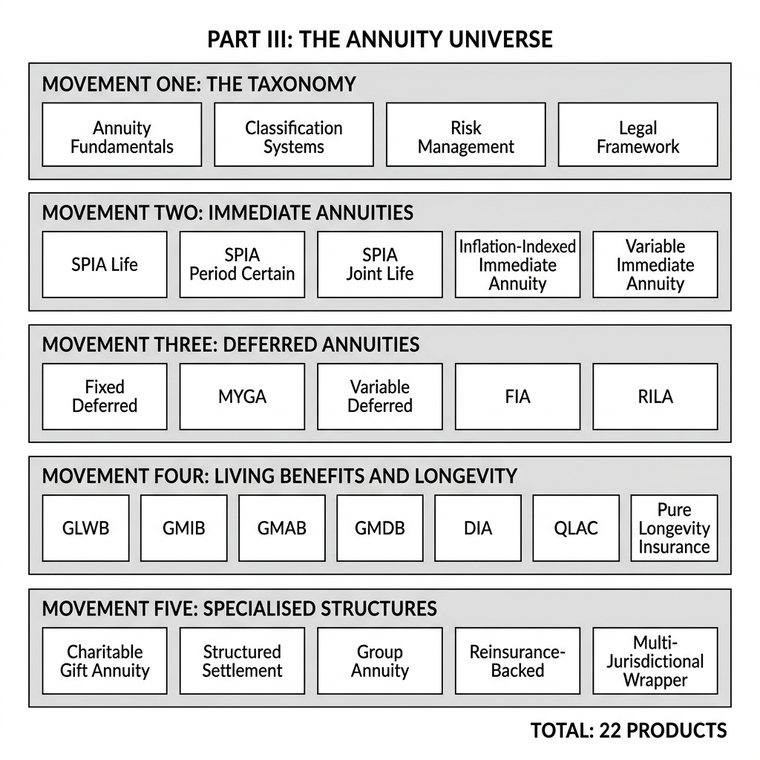

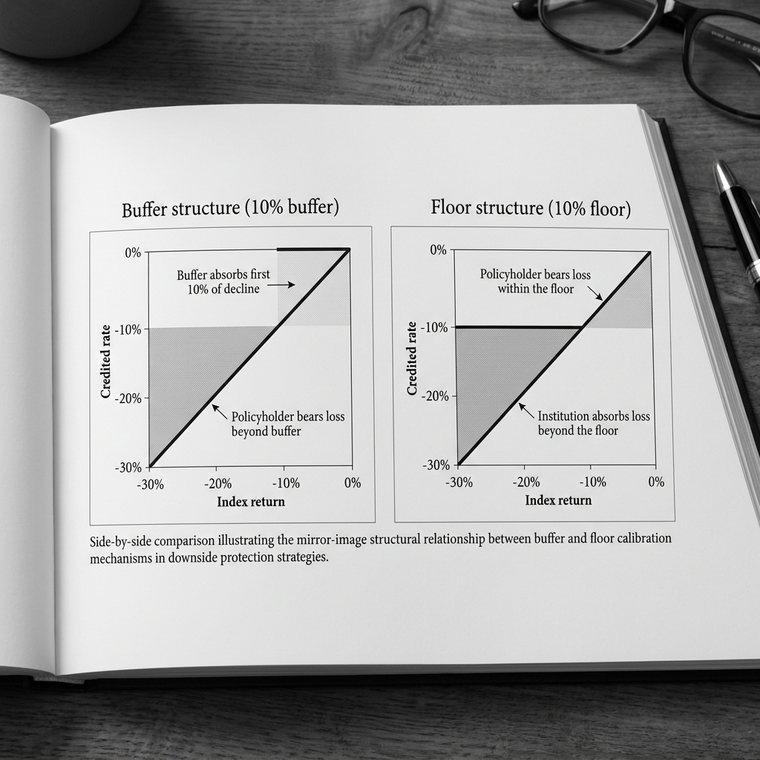

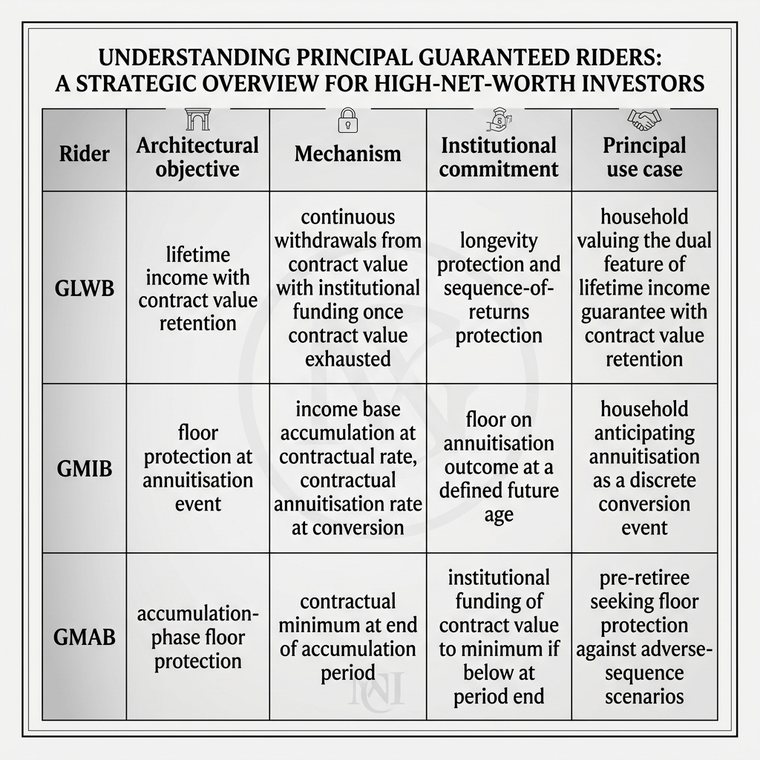

Immediate, deferred, variable, indexed, guaranteed, rider based, joint life, period certain, refund, and carrier quality structures.

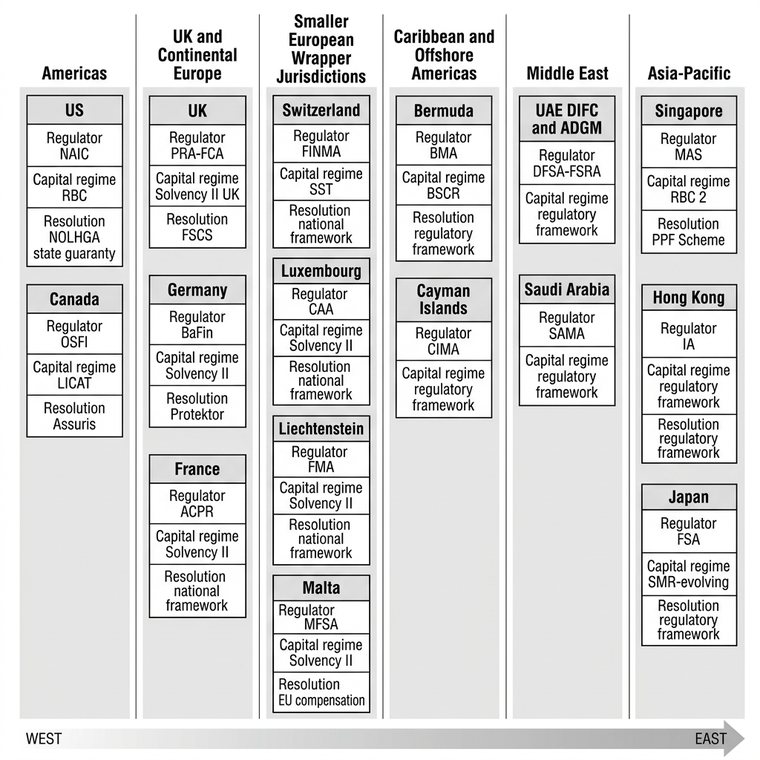

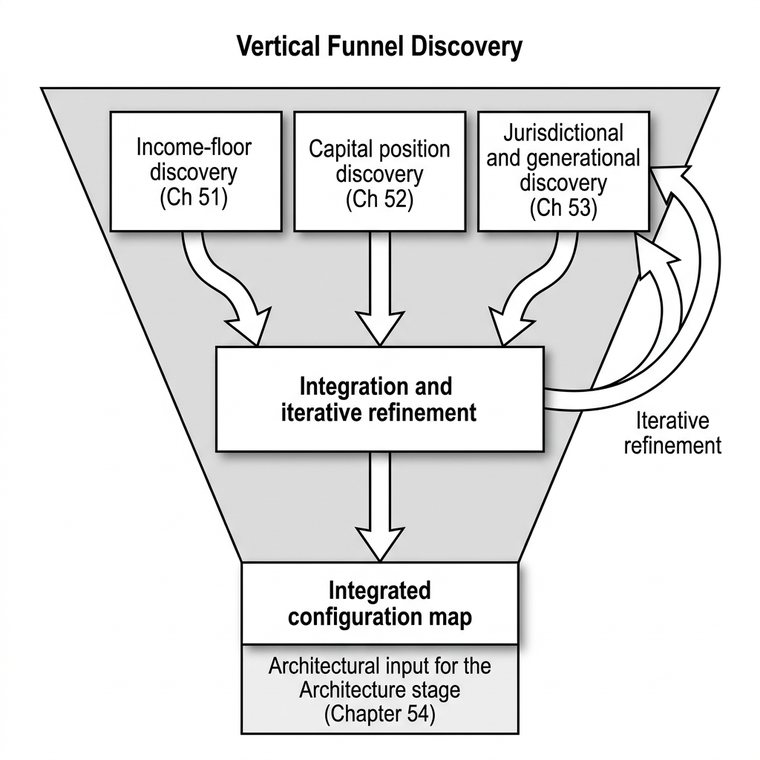

Configuration analysis, architectural design, institutional selection, legal establishment, contract placement, and long term stewardship.

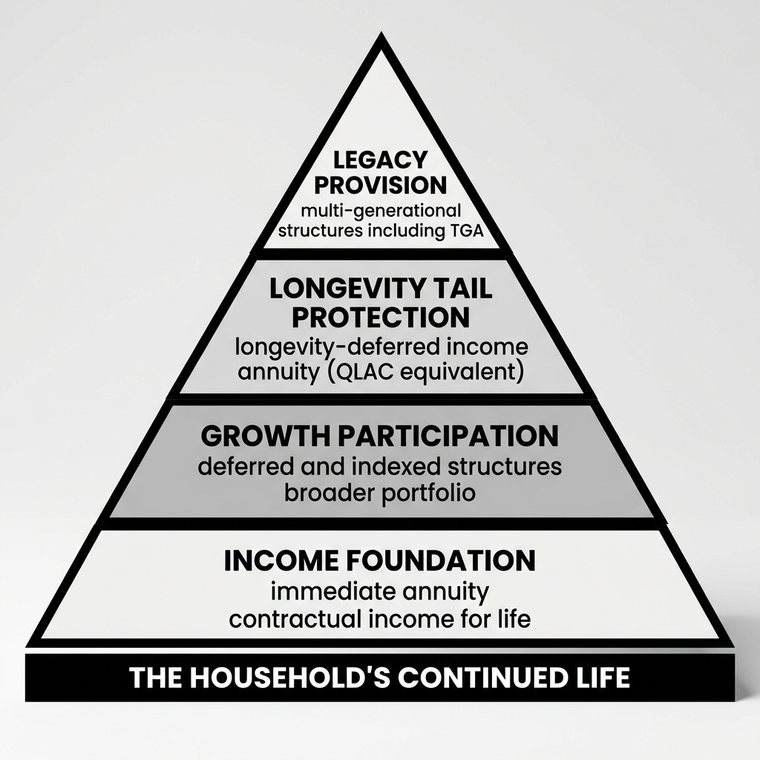

Four family situations that show how income architecture changes when the household, business, jurisdiction, and legacy objectives change.

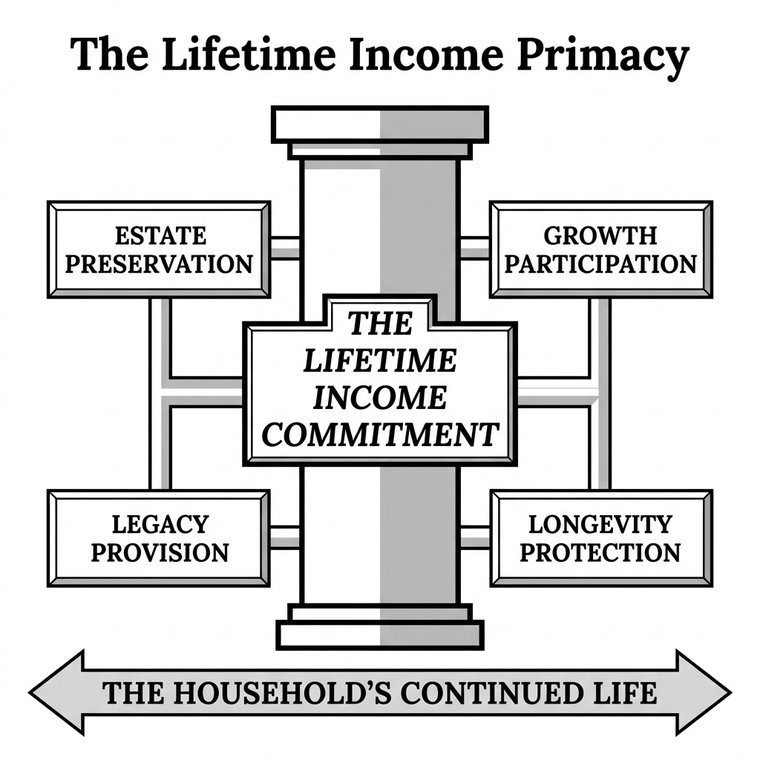

Retirement as a lifestyle, not an age. Work becomes optional when essential income is contractually secured.

Family office, corporate owned, charitable, cross border, Sharia compliant, single woman, widowhood, and closely held business configurations.

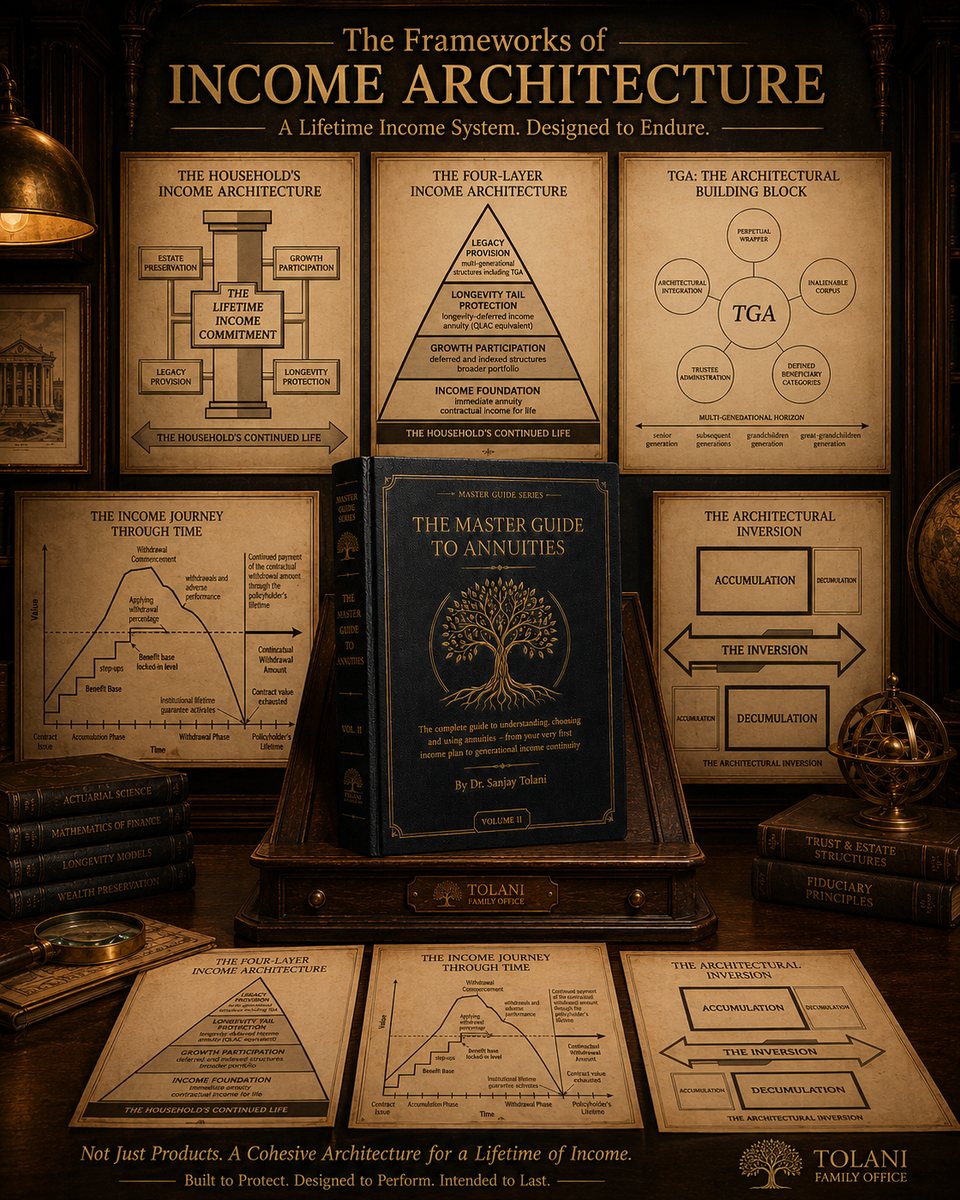

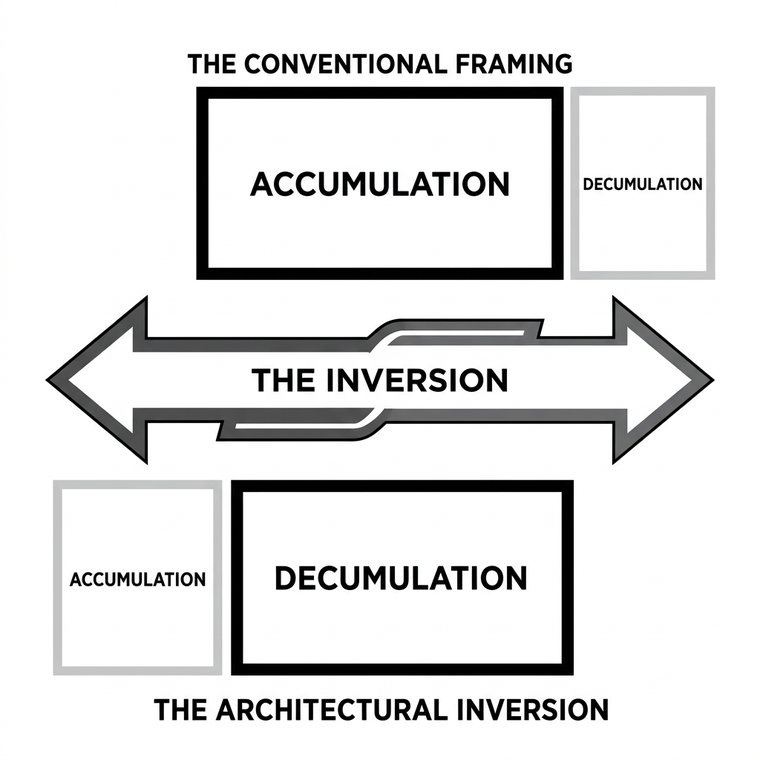

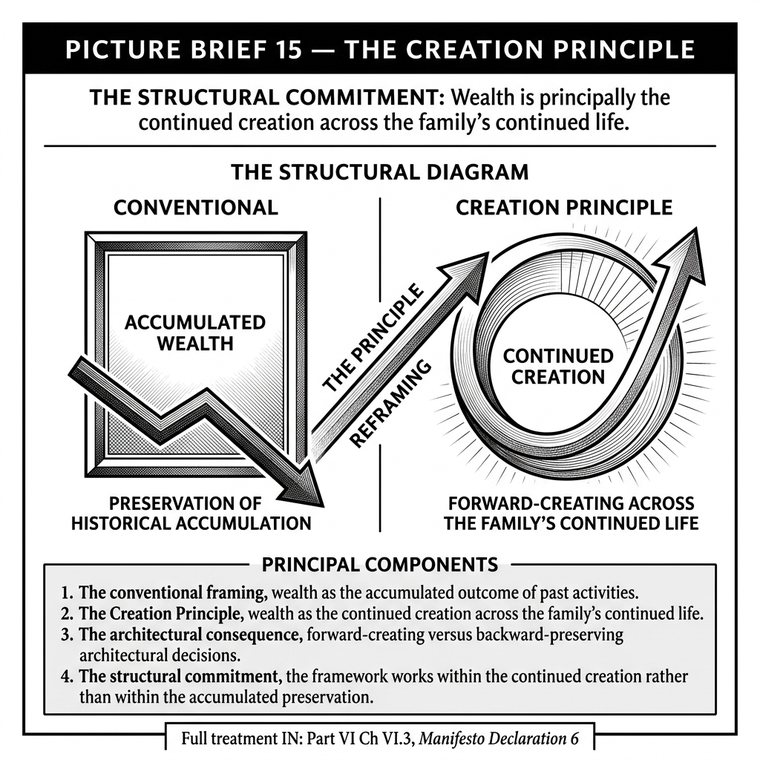

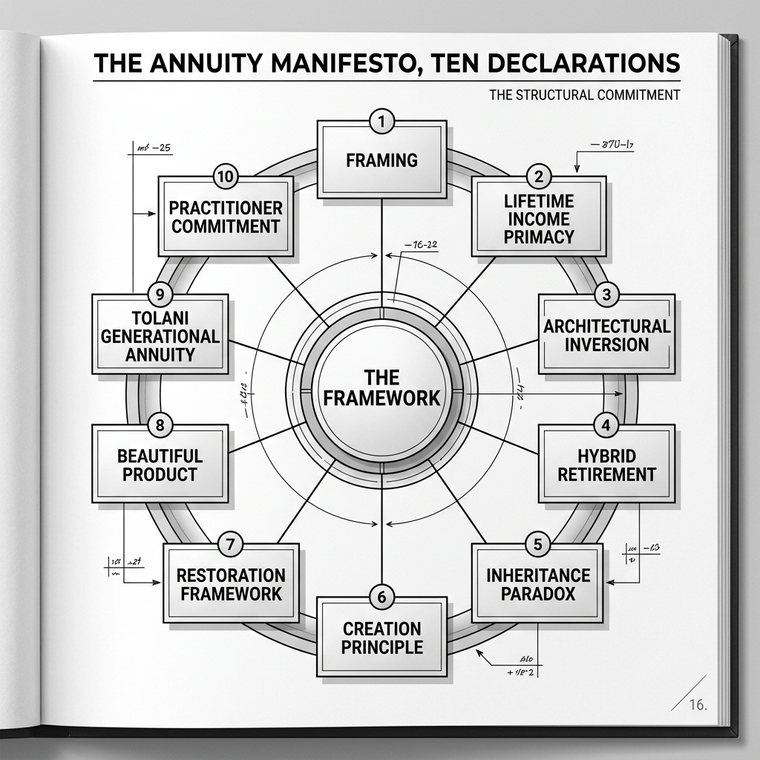

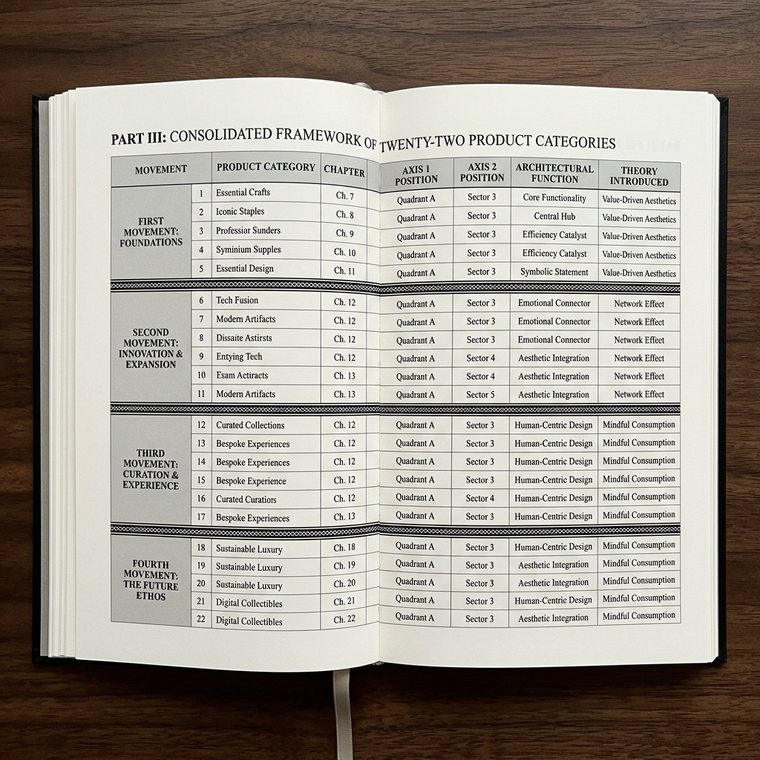

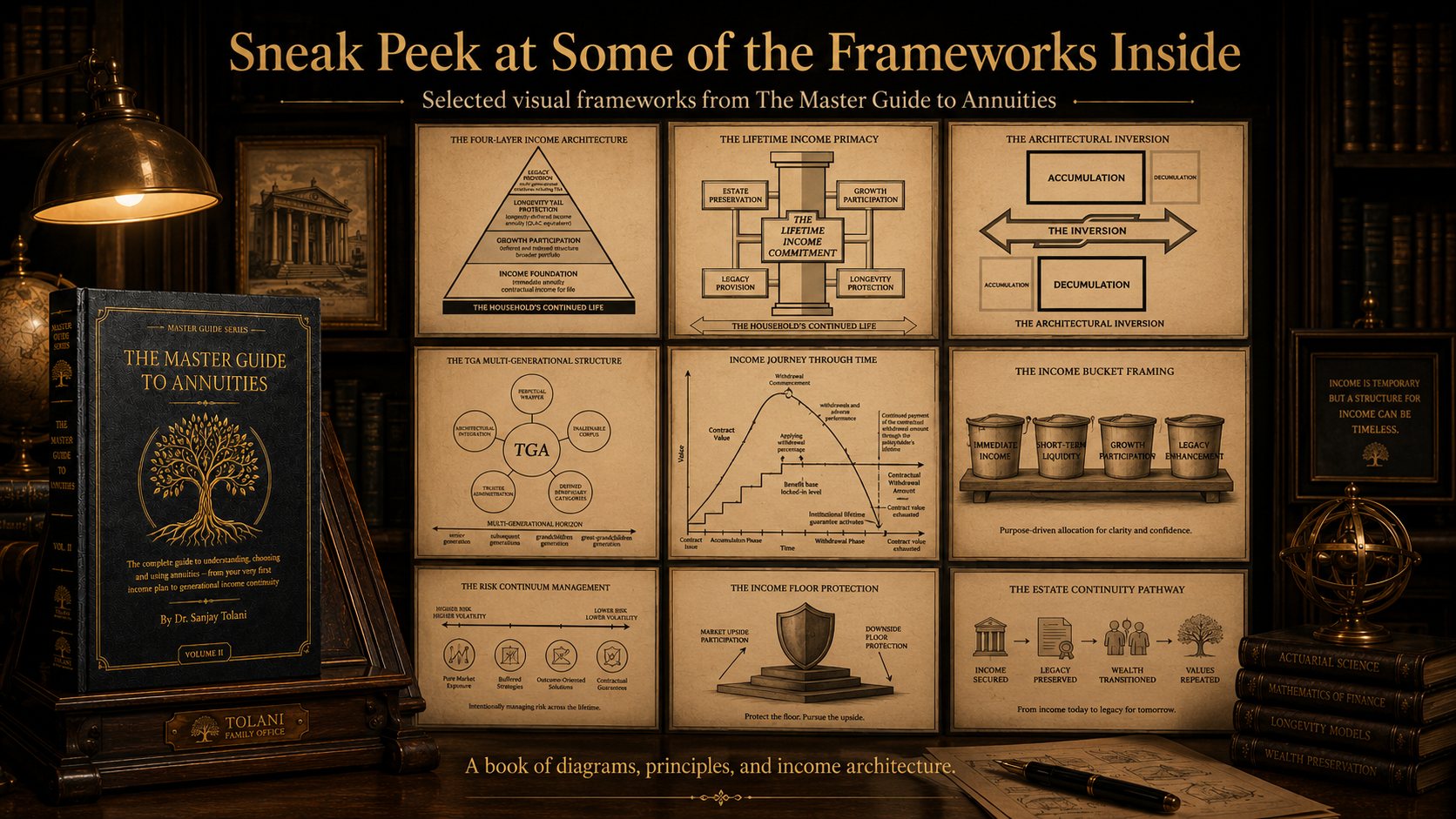

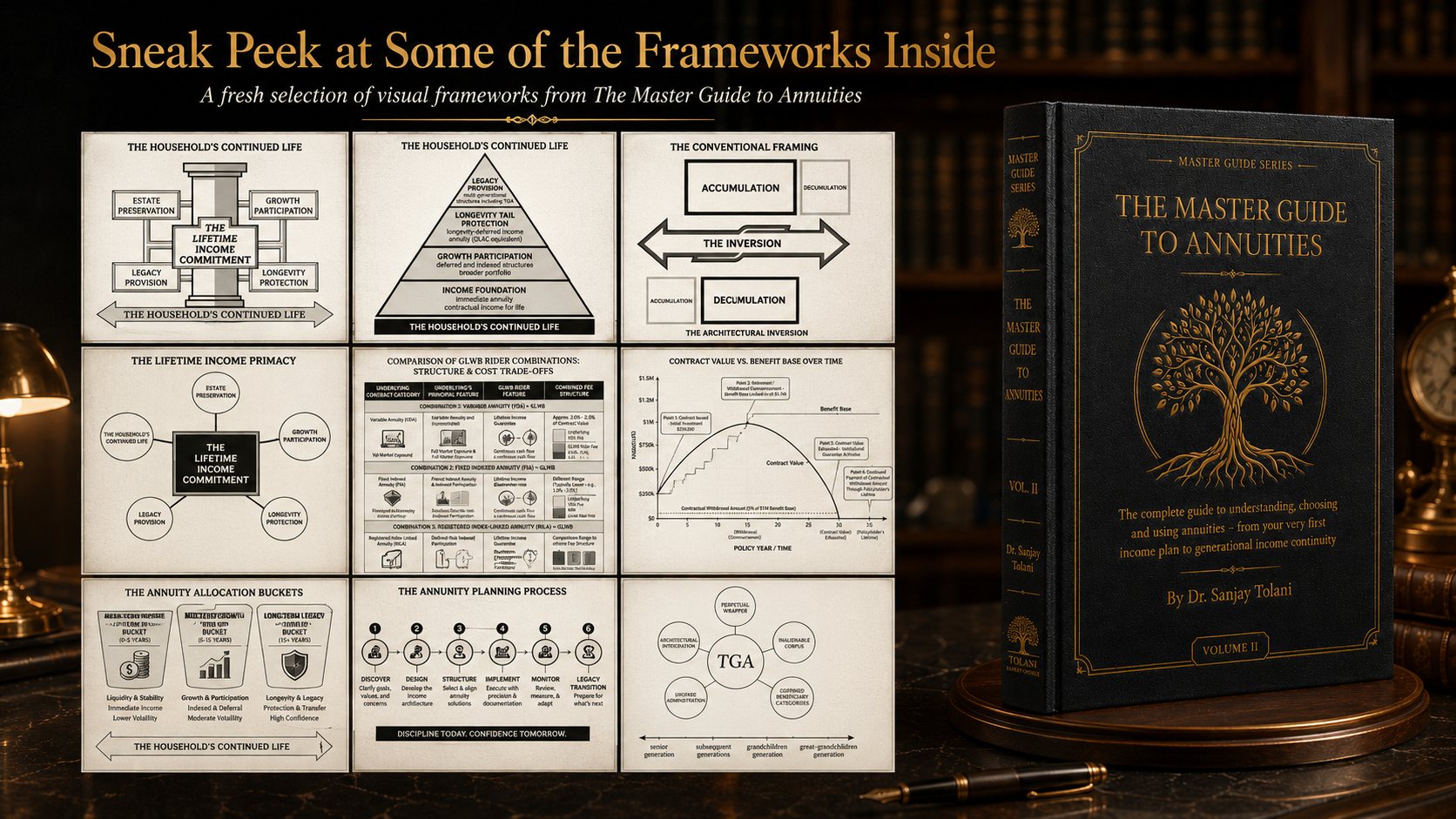

Not academic constructs. Distilled principles designed to survive long after the surrounding detail has been forgotten. Together, they form one visual, conceptual, and practical framework for understanding annuities as income architecture, not just product selection.

The 102 theory cards turn the book into a visual map. Each card captures one principle, one framework, or one recurring family situation from the volume.

These are actual framework images prepared for the book and website, converted into a gallery format for visitors who want to feel the depth before they read.

Hybrid Retirement is the lifestyle of someone who can stop, but chooses to keep going. Consulting, mentoring, travelling, writing, advising, building, pausing, returning. The obligation to earn no longer defines the structure of life.

Filter by conceptual section or search by theory name. All 102 uploaded theory images are included below.

The book is practical enough for a buyer evaluating an annuity proposal and deep enough for a family principal or advisor thinking about multi decade, multi jurisdictional income design.

The book closes with a simple invitation. If you want a more serious, visual, and complete conversation about annuities, join the waitlist and be first to know when copies become available.

If this annuities volume is about income architecture, the life insurance volume is its essential companion on protection, wealth transfer, and legacy strategy.

Together, the two books give readers a broader map of how families, advisors, and business owners can think about continuity across life, retirement, and generations.